[ad_1]

Hello,

A personal update to kick off the year: I’ve joined Powerhouse, an ecosystem actor for MakerDAO that is building an AI-enabled DAO operating system and plug-in store. Governance and DeFi remain both core interests for me, and I’m excited about returning to the DAO world and building for MakerDAO. I’ll continue to research on MEV, lending and the rest of DeFi but be on the lookout for more governance-related content. And if you’re at ETH Denver or building in DAOs, get in touch.

– Chris

This issue of Dose of DeFi is brought to you by:

No need to open up five tabs to make an informed trade. Oku has advanced analytics, limit orders, and TradingView charts, all in one place for the best DEX experience. Website & Twitter

DeFi lenders came out of the market carnage of 2022 bruised but still functioning (which could not be said for their CeFi brethren). Just as crypto markets were crashing and demand for leverage was plummeting, the Fed added to DeFi lenders’ pain via its most aggressive rate-hiking campaign ever, sapping demand for the modest yields in DeFi. And then in March 2023, the fall of SVB and the depegging of USDC threatened to push all lending protocols underwater.

A year later and that fear has disappeared; DeFi lenders are flourishing. On-chain rates now look more like those in TradFi (thanks to some nudging from Maker), and a whole new crop of innovative products have broadened collateral base and diversified the risk offerings – something that’s certainly set to continue.

While DeFi trading collectively struggles to offer a product more competitive than CeFi, DeFi lending has already surpassed CeFi and offers more potential to grow into mainstream markets with higher yields. Thanks to higher rates, DeFi lending protocols are seeing an explosion of on-chain revenue that will be reinvested back into expansion into new markets. We don’t expect a bull market sugar high, but rather a shift away from the DeFi of the zero interest rate environment toward a new period of higher revenue and broader appeal.

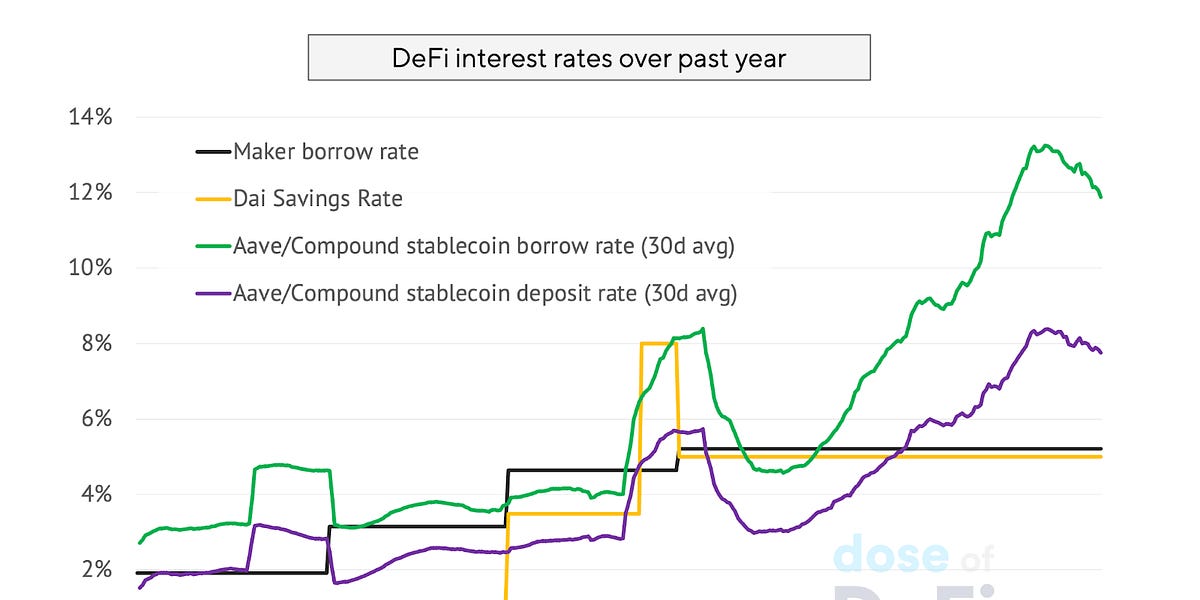

Rates climbed steadily throughout 2023, driven by two forces: the increased demand for leverage as markets heated up, and real-world yield coming on-chain. MakerDAO led the charge with higher rates when it voted to increase the borrowing rate for its vaults in the spring, even though demand for borrowing was tepid. Unlike Compound and Aave – where interest rates are set by market demand – Maker has full control over what interest rate it issues for Dai loans.

Maker was not raising rates just to stick it to borrowers. Higher lending rates allowed it to raise the Dai Savings Rate, first to 3.33%, and later to 5% (where it remains for now).

The growth of real World assets (RWA) in MakerDAO brought higher TradFi rates to DeFi and greatly reduced their stablecoin exposure. Dai was sometimes derisively mocked as “wrapped USDC”, but this is no longer the case. At the beginning of 2023, 63% of Dai was backed by USDC or another stablecoin. Fast forward to today, and that number is 12%. It has been replaced by real-world assets (primarily T-bills), which are yielding 5%+. This involves a lot of off-chain complexity swapping USDC in the Peg Stability Module for T-bills and dripping payments back to the protocol in Dai, but it scales better than crypto collateral.

Throughout 2023, Maker has maintained its lead in the ETH lending market ahead of Aave. In 2021, Aave benefited from an aggressive collateral onboarding strategy. This played out well for them in the transition to staked ETH, and their early mover advantage enabled them to lock in the liquidity network effects. It has more staked ETH than Maker. Staked ETH represents 59% of Aave’s ETH-based collateral, compared with 42% for Maker. Compound missed out on the staked ETH market, but remains a competitive second place (behind Aave) in WBTC.

MKR has led in token performance. Its standout growth, however, occurred over the past few months, on higher revenues from RWAs and speculation about changes in the Endgame (more on that later).

The close competitive dynamics between Maker, Aave, and Compound (and other smaller players) has helped drive a wave of continued innovation and new product releases in lending. This involves both new and old players alike. The most exciting recent developments are as follows:

-

Morpho launched in August 2022, and now has a couple of different products. The Optimizer is a P2P lending protocol built on top of Compound and Aave. It matches up lenders and borrowers directly and falls back on Compound or Aave. Just this month, Morpho released Morpho Blue, a protocol with a very thin layer of governance and off-chain dependencies. Instead of relying on core protocol governance to manage lending risks. Morpho Blue is permissionless at the base layer, but lending pools can be curated by DeFi service providers like Block Analitica, Steakhouse, or B. Protocol. It also offers higher loan-to-value (LTV) ratios due to enhanced capital efficiency.

-

Ajna just launched this month. It’s even more governance-minimized than Morpho and also boasts a non-oracle design, as well as being able to accept any ERC20 or NFT as collateral. It uses an internal order book for lending positions, meaning users sets a market price for what their collateral could solve for. Ajna could be thought of as an “interest-bearing limit order on the borrowed asset”. It’s not very normie friendly, but its flexibility means that others might build primitives on top of Ajna to make it easier to access for less sophisticated users.

-

GHO & crvUSD are new stablecoins from Aave and Curve respectively. GHO remains small (market cap: $35m) and has struggled with peg management. It’s still early days though, and given Aave’s position in the lending market, it can take its time building up an ecosystem around GHO. Presumably, Aave is interested in replicating the RWA model that Maker has pioneered. That’s not the case for crvUSD. Its strategic advantage is that it makes LPing on Curve more attractive, and there’s some reflexivity to it as a stablecoin hub. Its key innovation its slow liquidations. They just announced additional lending plans this week with code already up on github.

-

Spark is a fork of Aave v3 that was launched as a subDAO of MakerDAO. It is plugged into Maker core through the Direct Deposit Module (D3M). Unlike Compound v2 or Aave, the Maker Protocol is not a money market and does not lend out collateral (it uses the CDP model). Spark is a way of offering this product while still connected to Maker’s balance sheet. Spark’s Dai borrow rate is set by MakerDAO governance (currently 5.53%). It offers the best borrowing rates because it’s not dependent on its supply of Dai deposits. It can simply mint new Dai. Spark is just the beginning of some major changes to MakerDAO that revolve around the ambitious Endgame plan. For example, Spark will be one of several “subDAOs” that can borrow on Maker’s balance sheet. These subDAOs will have new tokens to be farmed out, starting this year. Maker is also getting a complete rebrand and a new token. The farming and rebrand should bring much needed attention to DeFi.

Additionally, lending protocols have seen significant growth in deposits and borrowing on their L2 deployments. Token emissions are a big reason for this, but the assets are likely to stay after incentives as interest rates on L2s are also relatively competitive with Ethereum. L2s and low-cost chains are very important for DeFi lenders’ expansion, as it’s the only way they can move towards a more mass retail investor base.

In DeFi, market dynamics are more fluid in lending, and success seems more dependent on catching the latest wave of investor preference. Compound’s early success was due to COMP farming, which kicked off a wave of copycats. Aave pulled ahead because it cornered the LST market.

Looking ahead, lending protocols will next be battling to attract the upcoming onslaught of restaked ETH tokens expected to hit the market with the launch of Eigenlayer. We discussed the “ETF-ization of ETH yield” last year and since then, several projects such as Rio, Renzo, and Swell, have already announced plans to launch new forms of tokenized restaked ETH. This will be trickier than staked ETH, where there are different tokens for the same yield (ETH rewards from the Ethereum protocol). With restaked LSTs, there will be scores of different types of yield with different risk considerations. The market will likely be more splintered than vanilla staked ETH, where Lido has 70%+ market share. Most interesting will be to see how conducive lending protocols are to highly-leveraged recursive borrowing, given that the asset prices of the restaked LSTs will be highly correlated, even if their risk is not.

Yield is a powerful motivator for investors. For the crypto-curious, DeFi’s high rates can be easy to write off as coming from “fake governance tokens”. But yield can also be pure, as demonstrated by the appeal of 5% risk free in TradFi last year. DeFi lenders could be the key to onboarding more casual DeFi users if they can offer sustainable yield. A significant amount of capital could flow from CeFi crypto users alone, if yields are attractive.

The most promising aspect of DeFi lenders is that they’re making money. MakerDAO could reach $200m in revenue this year, with expenses under $30m. Aave, meanwhile, may see $35m in yearly revenue, while Compound could surpass $15m. These are going to the DAOs and can be reinvested into growth and protocol development. Allocating that capital to entities that are aligned on a strategy and mission will require effective and efficient governance. Lending protocols have professionalized their risk management through service providers like Gauntlet, Block Analitica, and Chaos Labs, but they’ll need to extend this focus to other governance areas going forward. Lending protocols are complex and require coordination, but the last few years have proven that the model truly can scale and be a sustainable business model.

-

Bloxroute product to help validators navigate consensus timing games Link

-

What it takes to be a block builder Link

-

Flash market making MEV protocol Aori launches on Arbitrum Link

-

Paypal participates in CRV bribe governance for its stablecoin Link

-

Khlani Network aims to be decentralized solver infrastructure layer Link

-

Orderflow.art Link

-

Optimism RetroPGF Round 3 recipients Link

-

Synthetix launches v3 perpetuals on Base Link

That’s it! Feedback appreciated. Just hit reply. Written in Nashville, where I’m still recovering from our big snow last week.

Dose of DeFi is written by Chris Powers, with help from Denis Suslov and Financial Content Lab. I spend most of my time contributing to Powerhouse, an ecosystem actor for MakerDAO. All content is for informational purposes and is not intended as investment advice.

[ad_2]

Source link